Pensions, a self-employed secret weapon

When you’re self-employed, you quickly learn how to get the most from your budget. After all, it’s your hard earned money.

Eeking out a higher margin. Maximising any advertising spend. Tweaking dividends vs. salary. Each small decision has big consequences for your bottom line.

You do everything you can to maximise your return. The question is, why do you do all this only to lose so much to tax?

Luckily, you have a little-known ally in your quest. Your pension.

Pension Basics

Ok, let’s start at the beginning. Pensions are a confusing area and not everyone knows what they are or how they work.

A pension, put simply, is a tax-efficient way to save for retirement. For most, when they think of pensions they think of the state pension. This is a yearly income paid to you from the government when you reach retirement age (currently set at 68).

To qualify for a state pension, you need to have paid national insurance for 35 years - at which point you can receive a maximum of just £175.20 a week - a little over £9,100 a year. For the majority, this simply isn't enough.

A private pension refers to any type of pension that isn’t the state pension. There are main two types:

- Workplace pensions

- Personal pensions

If you've worked for an employer in the past, chances are you were enrolled in a workplace pension scheme. You may have forgotten that these old pension pots exist.

As someone who is self-employed, you’ll want to know about personal pensions. A Self Invested Personal Pension (SIPP) is a type of personal pension. A SIPP is what we offer at Penfold, as it allows for flexible investing and gives you the most control over where your money is invested.

With a SIPP, you can make ‘personal’ or ‘employer’ pension contributions, or you even mix between the two. Your money is invested in a fund of your choosing where it can grow tax-free, ready for when you reach 55 years old (or 57 after 2028).

Right, this all sounds great, but your retirement might be a long way off. Why should you worry about a pension now when there are so many other things you need to pay for? Two words: Tax. Relief.

Why Pensions Matter

Working for yourself leaves you short on time - it’s no surprise that planning for retirement quickly falls down your list of priorities. But what if there was a way for you to benefit from a pension, today?

Currently, it’s estimated that only 14% of the UK’s self-employed contribute into a pension. The outcome? A large proportion of those driving the UK economy simply aren't taking advantage of the benefits of saving for their future, with a 2018 study by the Department for Work and Pensions and IPSE declaring a ”pension’s crisis” for the self-employed.

But here’s the real issue: We estimate that around £1 billion in tax relief is left unclaimed each year because not enough people know about the benefits of paying into a pension.

We’re here to breakdown exactly how you as a self-employed worker can dramatically reduce your tax bill with a pension.

How Pensions Reduce Tax

First, you’ll get to take advantage of the tax relief at source. A ‘personal contribution’ into your pension saves you 25% in tax relief.

Let’s say for example you add £1000 into your pension. The government will add an extra £250 - this is because you’ve already paid £250 tax (at the basic rate of 20%) on the £1000 you contributed into your pension.

The government incentivises people to pay into private pensions by offering vast tax breaks on anything that add up to the yearly limit. As a Penfold pension customer, we claim this tax relief for you without you having to fill any forms.

But that’s just the start.

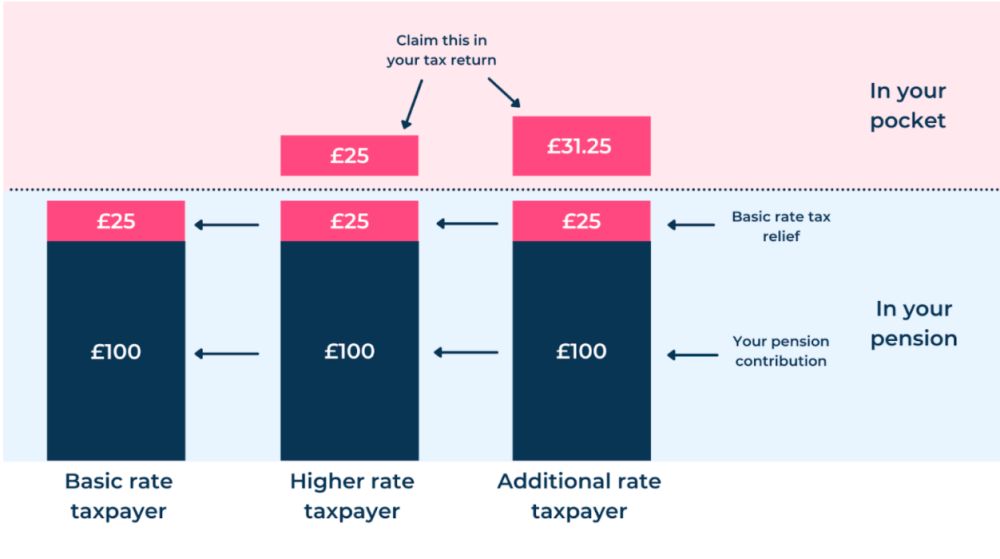

Extra Benefits for Higher Rate Tax Payers

If you are a higher or additional rate taxpayer, you can enjoy even more tax relief. Your contributions into your pension will automatically receive the 25% tax relief, but because you’re paying higher rate tax above the basic rate threshold, the government will pay back the tax you’ve already paid by offsetting it against your self-assessment tax return.

This means that contributions of £1000 into your pension will have £250 added on top by HMRC, and you’ll also be able to claim an extra £250 in your self-assessment tax return.

You can see an example of what that looks like in this graph.

How Much Could My Pension Save Me?

When you’re deciding how much to contribute into your pension each year for tax relief, it’s important to take into account your annual and lifetime allowances.

For most people, tax relief on pension contributions are capped at either their salary, or £40,000 whichever is lowest.

There is also a limit to the value you can save into a pension, called the Lifetime allowance or LTA. Currently, the LTA is £1,0731 million.

It’s important to bear this in mind when you’re contributing into your pension pot. Exceeding this allowance and triggering the 55% charge can cancel out any tax benefits you’ve accrued over the years!

Conclusion

Pensions aren’t just a long-term investment to set yourself up for the future. They’re also a fantastic way to make sure you keep more of your hard-earned profits today.

At Penfold, we’ve built the first ever pension designed for the self-employed. It’s easy to use, flexible and only takes a few minutes to set up - no paperwork required!

Start saving and top up, change or pause payments at any time with a few quick taps. No waiting lines and no call centres. Plus, our highly trained UK-based team is available 24/7 to answer your questions in our live chat app.

We’ll even help you transfer your old pension pots into one, easy to manage place. Get a pain-free pension today with a £50 free top up from us when you sign up using code: superscript!

About Penfold

Penfold is the digital pension provider designed for modern company directors. Set up an easy to use, flexible pension in minutes using your phone or laptop.

Penfold helps thousands of directors everyday by providing all the tools, calculators and information you need to make tax efficient decisions for your future. We've partnered with the largest money managers in the world to make investing your pot effortless.

We are regulated by the Financial Conduct Authority and our customers’ pension holdings are protected by the Financial Services Compensation Scheme.

This content has been created for general information purposes and should not be taken as formal advice. Read our full disclaimer.

We've made buying insurance simple. Get started.

- 27 May 20252 minute read

Superscript partners with Toolstation

We've teamed up with Toolstation to provide its members with business insurance built for their trade. Find out more.

- 26 September 20244 minute read

Pensions, a self-employed secret weapon

Pensions are a confusing area and not everyone knows what they are or how they work. We've covered the essentials to help you get more bang for your buck.

- 13 September 20246 minute read

A guide to National Insurance for the self-employed

Freelancers and the self-employed pay their National Insurance contributions a little differently to people employed by a company. Read our guide to the ins and outs of how National Insurance works for the self-employed.